Published February 17, 2010

The Republic must swiftly improve its personal-tax regime to make high-calibre individuals want to settle down here

By OOI BOON JIN

The Republic must swiftly improve its personal-tax regime to make high-calibre individuals want to settle down here

By OOI BOON JIN

YOU have probably read about the recommendations of Singapore's Economic Strategies Committee (ESC) and its vision of transforming Singapore into a leading global city.

As Singapore stands at the crossroads of reinventing itself, the upcoming Budget next Monday promises to be an exciting indicator of the government's plans to lay the groundwork for this exciting future.

Key among the ESC's proposals is making Singapore a Global-Asia Hub. In line with this goal, is recognising the importance of complementing Singapore's workforce by attracting highly capable and entrepreneurial people to Singapore.

The very recognition of their capabilities suggests that these people are likely to possess highly sought-after skills, know-how or other abilities. They are therefore likely to be highly sought after not only by Singapore, but many other countries.

They are therefore highly mobile and have numerous choices as to where to locate. In Asia, besides Singapore, Hong Kong is often the other location that ranks high on their list of options.

Corporate concerns aside, while each country's tax authorities may want an overall fiscal policy which enhances their country's competitive landscape, the importance of personal tax policy as a deciding factor should not be overlooked.

For many high-calibre individuals, attracting the companies they work for to Singapore must also include another dimension: the location must appeal to them on both the rational and emotional levels.

These high-calibre individuals therefore provide important input into the decisions their companies make on where to locate them - their regional headquarters or branch office.

Besides the usual medley of concerns such as quality of life, amenities and the environment, the personal tax regimes of the countries they are considering could potentially make or break the deal.

At the income levels that these individuals typically command, an uncompetitive personal tax rate may be the proverbial straw that breaks the camel's back. This is especially so when personal taxes directly hit the pockets of the people concerned.

At the income levels that these individuals typically command, an uncompetitive personal tax rate may be the proverbial straw that breaks the camel's back. This is especially so when personal taxes directly hit the pockets of the people concerned.

As businesses evaluate their costs of doing business in regional hubs such as Hong Kong and Singapore, the million-dollar question arises: is Singapore a match for Hong Kong in creating a low-personal-tax environment for high-fliers?

Let us measure Singapore against rival Hong Kong. It is interesting to note that our highest personal tax rate of 20 per cent is dismally short of closing the tax gap with Hong Kong, which has a flat rate of 15 per cent.

Coupled with some significant deductions given in Hong Kong - such as home loan interest - Hong Kong's personal-tax regime seems to have the upper hand.

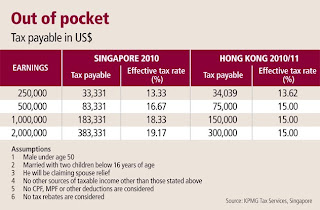

Singapore versus Hong Kong

Based on several scenarios and assumptions, KPMG's projections of the variance between Singapore and Hong Kong suggest that the difference is very significant for the highest-earning taxpayers.

For example, a married expatriate individual earning US$2 million per year would pay taxes of US$300,000 in Hong Kong. In Singapore, his tax bill would be about US$383,000. The difference of US$83,000 is about four percentage points.

In a different income bracket, a married expatriate individual earning US$250,000 per year would have about the same take-home pay in Singapore and Hong Kong.

The major assumptions used in the KPMG computations include the following:

> Non-working spouse and two dependent children with its attendant reliefs and allowances

> No pension/social security contributions or benefits-in-kind

> No special tax deductions such as home loan interest.

Doing more for individuals

Singapore has come a long way in trying to bridge the tax gap for such individuals - for example, abolishing estate duty in 2008, as Hong Kong did a year before. This removed the stumbling block which discouraged both foreigners and Singaporeans from locating their assets here.

However, for individuals outside the income brackets illustrated, unless the reduction is in the magnitude of four or five percentage points a year, a smaller reduction may not be immediately felt.

Other measures that the government could therefore also consider include:

Fine-tuning the time apportionment concession under the Not Ordinarily Resident (NOR) scheme to be on par with Hong Kong's time apportionment basis, which does not have a five-year 'life' or a 90 overseas- business-day requirement.

Other measures that the government could therefore also consider include:

Fine-tuning the time apportionment concession under the Not Ordinarily Resident (NOR) scheme to be on par with Hong Kong's time apportionment basis, which does not have a five-year 'life' or a 90 overseas- business-day requirement.

Allowing a tax deduction for mortgage interest incurred by homeowners. Unlike their counterparts in Hong Kong and Taiwan, homeowners in Singapore do not get a tax benefit for the housing loans that they repay every year.

Continuously working to create a more competitive personal-tax environment is one tenet of Singapore's strategy for becoming an Asia Hub. However, it may also be timely to review and improve Singapore's personal-tax regime against that of Hong Kong. This is perhaps most critical in attracting the talents we want to have come and live here.

The writer is executive director and head of international executive services at KPMG in Singapore. The views expressed herein are those of the writer and do not necessarily represent the views of KPMG in Singapore

The next interesting point is 7,286, the low of 2002, when the rally began. According to Russell, if the Dow holds at 7,286 and begins a rally, this might be a good time to buy. But if it fails to hold at 7,286 and slides past 6,547, then look out for dead cats dropping from the sky. Russell predicts that Dow 1,000, the number at which the Dow began its rally in the 1970s, may not be out of the question. If that happens, there will be millions of baby boomers joining the dead cats falling from the sky as their 401(k)s and IRAs implode.

The next interesting point is 7,286, the low of 2002, when the rally began. According to Russell, if the Dow holds at 7,286 and begins a rally, this might be a good time to buy. But if it fails to hold at 7,286 and slides past 6,547, then look out for dead cats dropping from the sky. Russell predicts that Dow 1,000, the number at which the Dow began its rally in the 1970s, may not be out of the question. If that happens, there will be millions of baby boomers joining the dead cats falling from the sky as their 401(k)s and IRAs implode.